.svg)

Not Everyone Is Trading The Same Oil

On February 28, US and Israeli strikes hit Iran on a Saturday. NYMEX, CME, and ICE were all closed. Oil perps on Architect 's AX exchange, Trade XYZ on Hyperliquid , and other venues never stopped trading. Trade XYZ's contract surged 5% to $70.60 a barrel within hours. By Monday's open, the price had already been set.

That moment showed something important. The tool and venue you use shape what you actually hold. Before picking a venue, answer two questions: which oil, and which tool?

The Benchmark Layer: There Is No Single Oil Price

Three main oil benchmarks exist:

→ WTI is a light, sweet crude priced at Cushing, Oklahoma and traded on NYMEX. It is the North American standard.

→ Brent is a blend of North Sea crudes. It prices over three-quarters of all traded crude globally.

→ Dubai/Oman is heavier and more sour. It is the main reference for Middle East oil flowing to Asian buyers.

These grades always trade at a spread to each other. When a product claims to track "oil", the benchmark it uses shapes the price signal you get.

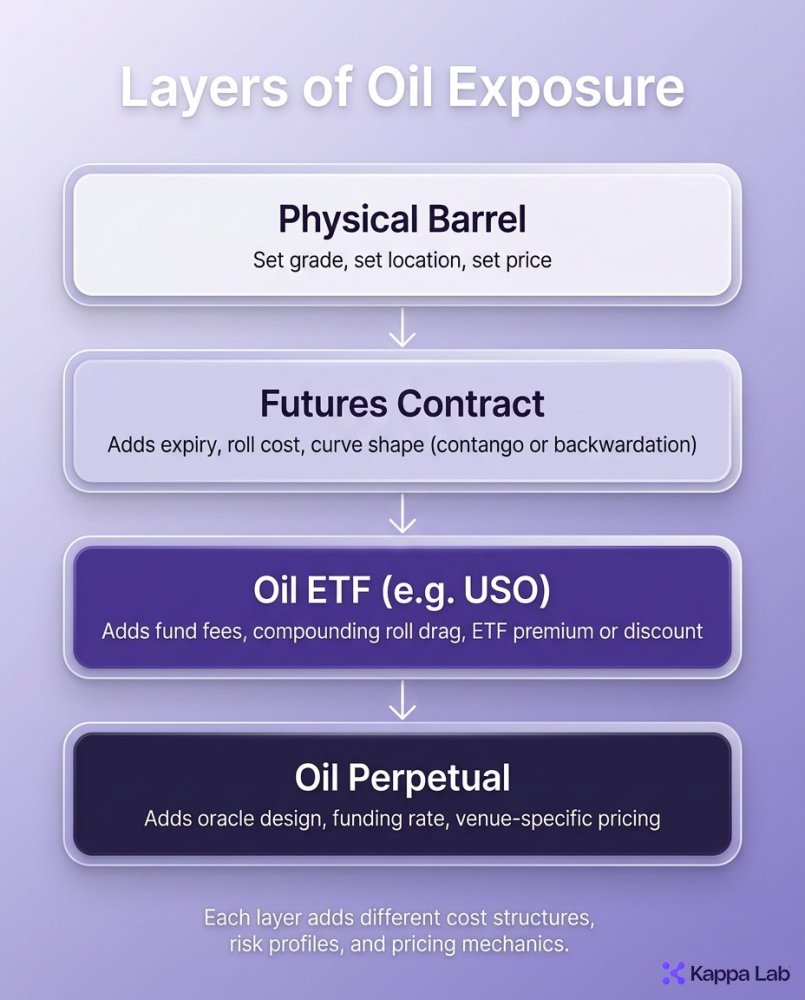

Traditional Futures: Physical Delivery, Rolling Expiry

Futures are the main pricing engine for physical crude. A standard WTI contract on NYMEX covers 1,000 barrels, delivered to Cushing on a set date.

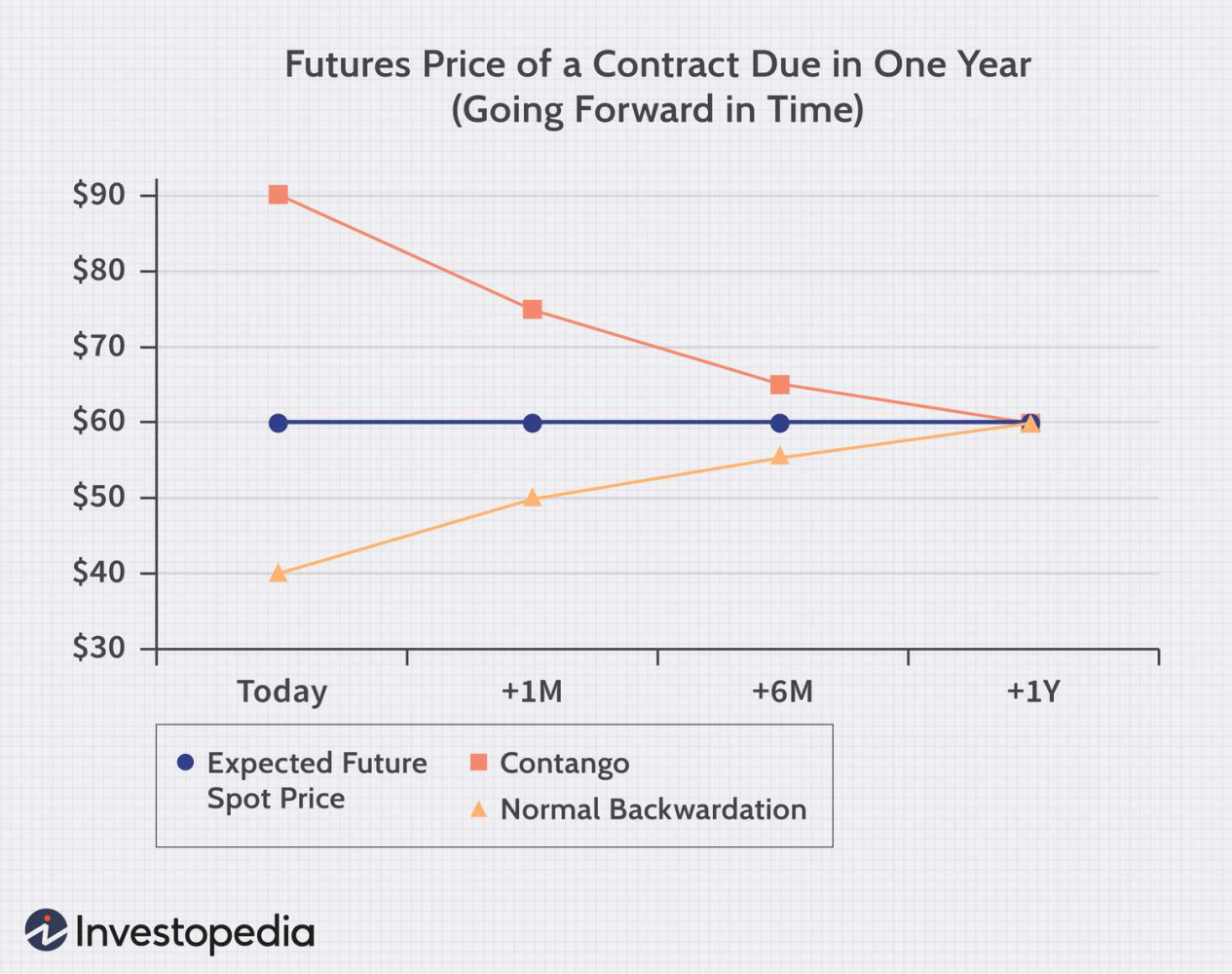

These contracts expire. Traders who want to stay in the market must roll into the next month. When far-dated contracts cost more than near ones (contango), each roll costs money. When near contracts cost more (backwardation), rolling earns a gain. The futures price always reflects both spot value and the shape of the curve.

ETFs: Synthetic Exposure, Compounding Roll Drag

Most retail investors access oil through futures-backed ETFs. A fund like USO holds front-month WTI futures and rolls them forward each month.

In contango, USO sells cheap near-term contracts and buys more costly ones. The drag builds up over time. During the 2020 oil crash, USO contracted roughly 75%, with no direct match in the physical market. ETF investors are as exposed to the curve's shape as to the oil price itself.

Oil Perps: No Expiry, But Not All the Same

Oil perps now trade across a growing number of venues. Each gives you ongoing exposure to oil with no expiry. But they are not the same product. The key question: what is the price feed actually tracking?

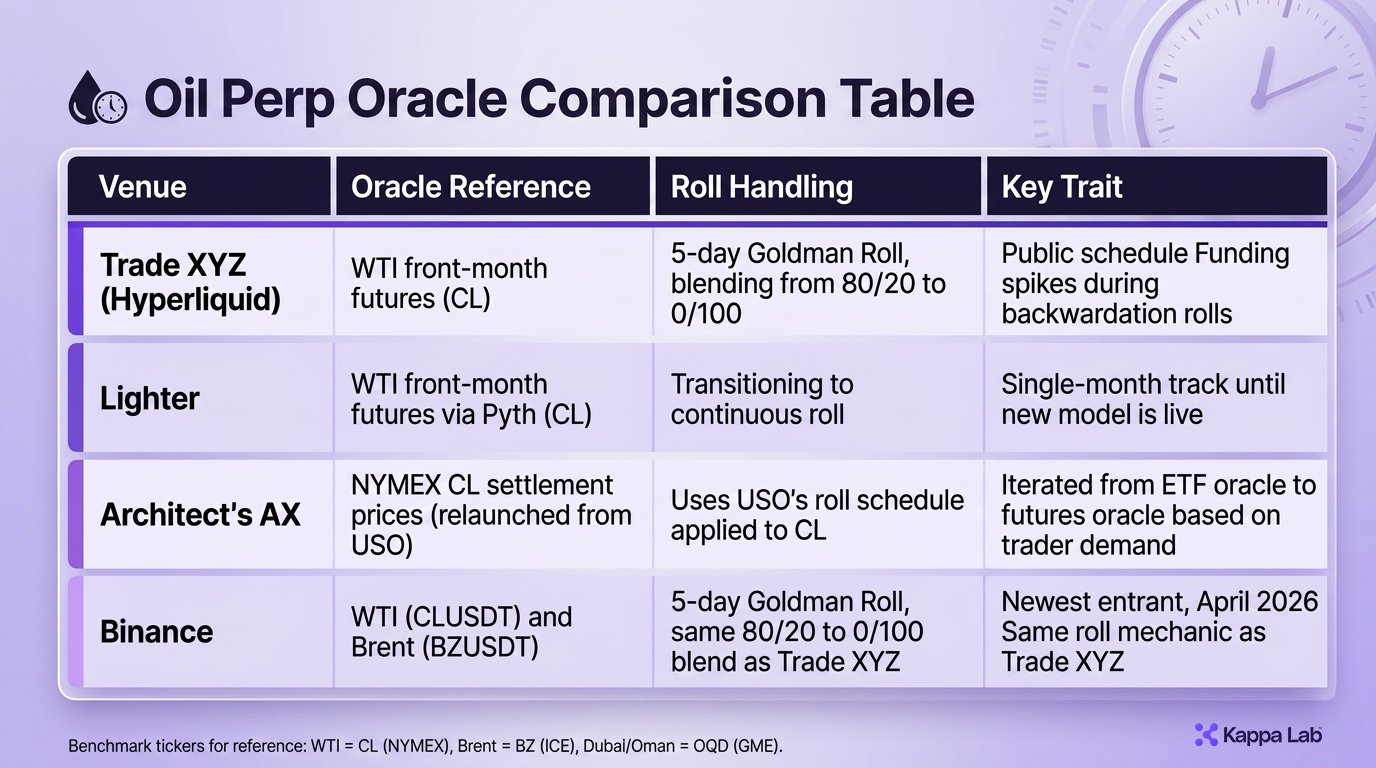

Trade XYZ on Hyperliquid tracks WTI front-month futures. To handle the monthly roll, it blends the old and new contracts over a five-day window, shifting weight from 80/20 to 0/100. The roll schedule is public and fixed.

What this looks like in practice became clear during the April 2026 roll. WTI was in steep backwardation, with the May contract well above June. Traders priced the perp at the June level early, creating a sticky discount to the front-month oracle. Funding rates spiked to around -400% on an annual basis. Shorts paid longs roughly 1% per day. The "obvious" arb of shorting the perp against a long June futures position was roughly wiped out by funding costs. The roll window was far less simple than it looks on paper.

February 28 was a live stress test for this layer. Per reporting on a JPMorgan note from March 2026, Trade XYZ's CL-USDC contract saw over $1.5 billion in peak daily volume during the crisis. Open interest rose to hundreds of millions of dollars. Leading price discovery, rather than just tracking it, makes oracle design and funding structure far more critical.

Lighter also tracks WTI front-month futures, using Pyth Network as its oracle. It is moving to a rolling model. Until then, the contract tracks a single futures month and shifts at the roll. Lighter also lists Brent and natural gas perps.

Architect went through this design question in real time. As CEO Brett Harrison put it:

"Building a perpetual whose funding rate is based on a futures contract leads to the fundamental question: what should the contract track as the front month approaches expiry? At first, we at Architect decided to base our exchange AX's crude oil contract on USO, the USCF crude oil ETF. USO has a roll procedure which smoothly transitions its basket from the front month to the back month over several days, in a manner that preserves the continuous value of USO's NAV. However, this contract proved unpopular as traders are much more used to understanding the price of CL on NYMEX vs the price of USO on ARCA. We have since relaunched our crude oil perpetual using NYMEX CL settlement prices directly, leveraging the same roll schedule as USO."

The shift shows that oracle design is not just a technical choice. It is shaped by what traders expect to see on screen.

Binance launched WTI (CLUSDT) and Brent (BZUSDT) oil perps in April 2026. The contracts are USDT-settled. For the roll, Binance uses the same approach as Trade XYZ: a 5-day blended transition shifting weight from the expiring contract to the next one. Binance calls this the Goldman Roll.

Four Instruments, Four Exposures

→ A futures contract gives you exposure to a set grade, at a set delivery point, on a set date.

→ An oil ETF gives you exposure to the roll costs of near-term futures, shaped by fund fees.

→ An oil perp with a futures oracle gives you ongoing exposure to a contract month, with oracle shifts at the roll.

→ An oil perp with an ETF oracle gives you exposure to the fund's price, with roll complexity handled upstream, though most venues now reference futures directly.

None of these are the same. The same asset can trade at different prices across venues at once, most visibly during roll windows and off-hours.

The Liquidity Dimension

Each layer has its own depth profile. Futures depth pools in front-month contracts. ETF liquidity tracks the futures market and retail demand. Oil perp liquidity runs all day but varies by session and venue.

For those active across these layers, the spread between them is the core problem. Basis risk, the price gap between two tools tracking the same asset, shows up in fills, hedges, and risk at the point of trade.

At Kappa Lab, we run liquidity where execution, risk, and these markets meet. We are active across venues and we work on the problems that come with providing steady liquidity across instruments that track the same thing but price it differently.

If you're building in this space and need reliable liquidity, reach out.

Your Liquidity?

.svg)

.svg)

.svg)

.svg)

Kappa Lab Capital FZCO is a proprietary trading firm registered in Dubai, UAE. It operates under a No Objection Confirmation (NOC) from the Virtual Asset Regulatory Authority (VARA).

The information on this website is not directed at nor intended for distribution to, or use by, any person resident in any country or jurisdiction where such distribution or use would be contrary to local law or regulation. The content on this website is for informational purposes only and should not be considered an offer or solicitation to engage in any financial activity.