.svg)

Strategy's Bitcoin Funding Engine: How STRC became the base layer for wrappers, yield markets, leverage, and perps.

Strategy (formerly MicroStrategy) has raised over $8 billion through a single preferred stock in under nine months. Most of that capital went straight into Bitcoin. That same instrument now sits at the foundation of an onchain capital stack: tokenized wrappers, yield-stripped tokens, leveraged loops, and a perpetual on a DEX.

Here's what's happening, and why it matters.

The Instrument

STRC (Stretch) is Strategy's Variable Rate Perpetual Preferred Stock. It carries a $100 stated value and pays monthly cash dividends. Each month, the board adjusts the rate based on how STRC is trading relative to par.

The system works on a simple scale. If the five-day average price drops below $95, the rate goes up by at least 50 basis points. Between $95 and $99, it goes up by 25. Above $101, it goes down by 25. The goal: keep STRC pinned near $100 and strip out the wild swings of MSTR common stock.

STRC launched via IPO in July 2025 at $90 per share with an initial rate of 9%. The rate has been raised seven times since, reaching 11.50% by March 2026. April was the first month it held flat.

The Numbers

SEC 8-K filings and data from strc.live tell the story. STRC has raised $8.25B in net proceeds from 85.37 million shares sold across the IPO and 15 ATM rounds. Those proceeds funded an estimated 98,843 BTC at a weighted average cost of $83K. The instrument's market cap sits at $8.49B.

The pace of buying has changed sharply. From the July 2025 IPO through January 2026, total BTC bought through STRC sat at around 25,000. By late April, that figure had nearly quadrupled. The two biggest weeks: $1.18B (March 8–14) and $2.18B (April 12–18), both funded entirely through STRC with zero MSTR common share dilution. STRC accounted for 86% of the $2.54B raised in the April 13–19 period alone.

As of April 26, 2026, Strategy holds 818,334 BTC. Total cost: $61.81B. Average price: $75,537 per coin. The instrument cycles between active issuance and pauses: the week of April 20–26, STRC's ATM was on standby and Strategy bought just 3,273 BTC, funded by common stock instead.

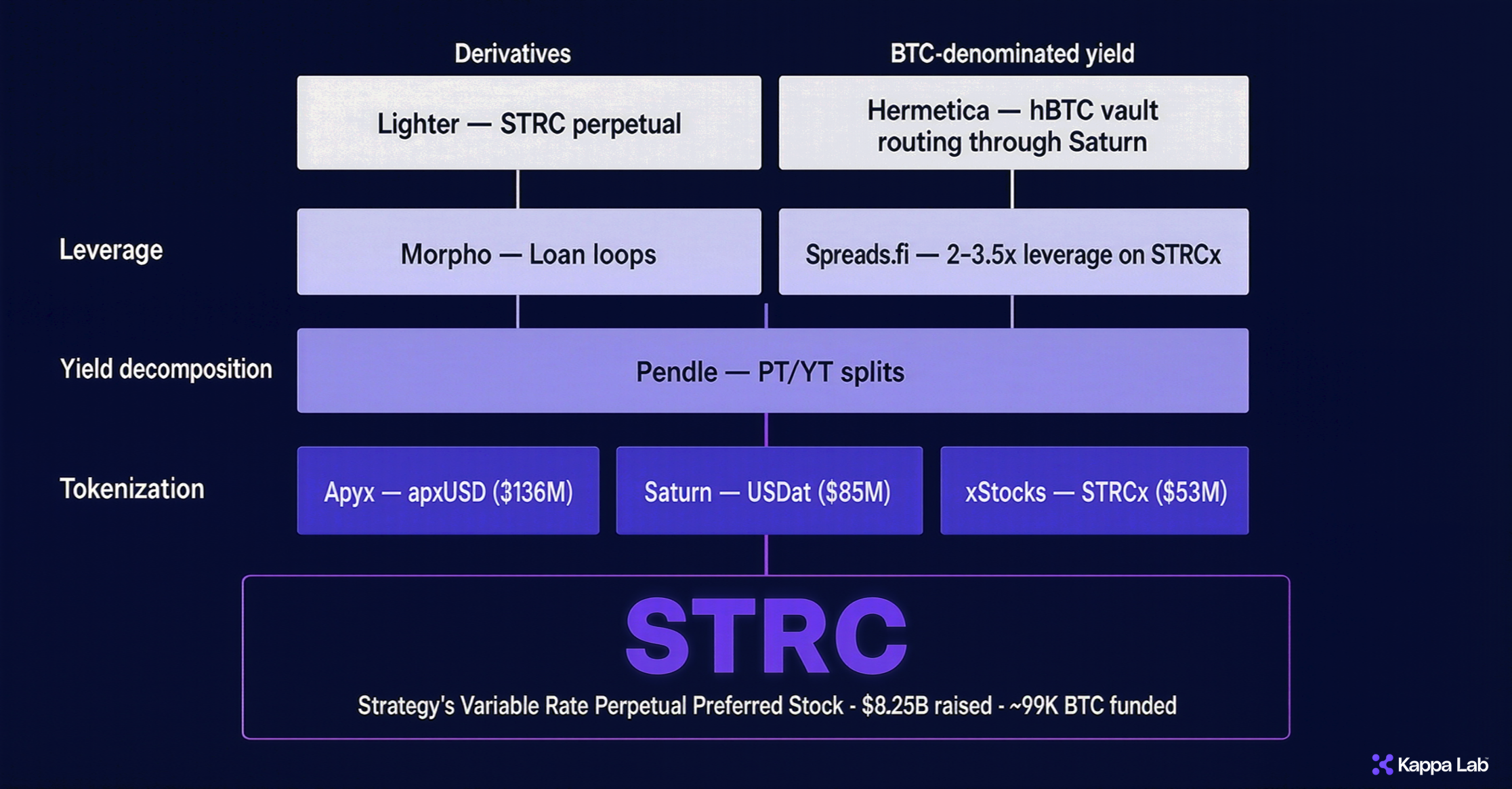

The DeFi Stack on Top

In under nine months, an entire onchain capital stack has formed around STRC. The visual above maps it; the prose walks through each layer from the base up.

Tokenization

Three protocols wrap STRC into stablecoin-like tokens. Apyx packages roughly $136M into apxUSD, with apyUSD as the staked, yield-bearing version. Saturn Credit wraps about $85M into USDat and sUSDat. xStocks tokenizes another $53M as STRCx, an onchain version tradable on DeFi rails.

Yield decomposition

Pendle splits these tokenized products into principal and yield components. Holders can lock in fixed rates or speculate on the variable dividend stream separately. PT-apyUSD has been quoted at fixed yields near 15%.

Leverage

Morpho enables loan-looping: deposit a tokenized STRC product, borrow stables, redeposit, repeat. A 5x loop on PT-apyUSD has been reported to produce yields north of 60% APY. Spreads Finance, launched April 21 on Ink chain, offers 2-3.5x direct leverage on STRCx with advertised APYs above 20%.

Derivatives

As far as we are aware, Lighter is the first perp DEX to list an STRC market, giving traders direct short and leveraged exposure to Strategy’s perpetual preferred stock.

BTC-denominated yield

Hermetica 's hBTC vault on Stacks routes BTC deposits through Saturn's sUSDat to deliver Bitcoin-denominated yield, completing the loop back to BTC for holders who want exposure in their native unit of account.

Where The Seams Show

The spot/DeFi pricing gap is no longer theoretical. On April 14, STRC went ex-dividend and dropped below par for the first time, hitting $99.06. Each month, after Strategy snapshots holders around the 12th-15th, those who only wanted the dividend reduce exposure, pushing the price below par by roughly one month's yield.

This time, the dip leaked into DeFi. Pendle's yield accrual on YT-sUSDat paused: STRC's price decline pushed Saturn's exchange rate below Pendle's high-water mark, breaking the yield mechanic. Pendle issued a public note to users.

The Lighter perp shows the same gap from a different angle. Holders of the perp do not receive the spot dividend, so funding rates have to compensate. In a thin market with $362K in open interest, equilibrium is still finding itself.

Three days after the dip, Strategy proposed moving STRC dividends from monthly to semi-monthly, with the first split payment scheduled for July 15 if approved. The stated goal: dampen ex-dividend volatility. If approved, the monthly dip gets cut in half, changing the math for any DeFi product whose yield mechanic depends on the snapshot cadence.

The instrument has drawn substantial public skepticism. Peter Schiff has called STRC "the most obvious Ponzi that has ever existed," arguing that buyers are chasing the 11.5% dividend rather than Bitcoin exposure. Strategy maintains roughly $2.25B in cash reserves, covering approximately 30 months of payments at current rates.

The Broader Question

STRC is one answer to a basic problem in treasury management: if the treasury holds a volatile asset and bears the risk, who captures the return?

Strategy's answer is structured equity. The treasury holds Bitcoin. STRC turns that into a yield-paying product for a different type of investor. The upside (or downside) stays with common shareholders. The economics are split across the capital stack, not handed to outside parties.

This is not a unique problem. Token foundations face the same tension every time they sell volatility on their native holdings to generate yield. The upside often goes to outside parties. The downside stays on the balance sheet. The instruments are different. The question is the same.

This is the question our latest product Klip was built to address. Where Strategy uses structured preferred equity to keep treasury economics inside the capital stack, Klip does the same for onchain treasuries: tokens stay productive, custody stays with the protocol, the economics stay with the treasury.

At Kappa Lab , we operate liquidity infrastructure at the intersection of execution, risk management, and evolving onchain market structure. If you're building in this space and need reliable liquidity, reach out.

Your Liquidity?

.svg)

.svg)

.svg)

.svg)

Kappa Lab Capital DMCC is a proprietary trading firm registered in Dubai, UAE. It operates under a No Objection Confirmation (NOC) from the Virtual Asset Regulatory Authority (VARA).

The information on this website is not directed at nor intended for distribution to, or use by, any person resident in any country or jurisdiction where such distribution or use would be contrary to local law or regulation. The content on this website is for informational purposes only and should not be considered an offer or solicitation to engage in any financial activity.